")

Introduction

Best bank for mortgage loan in UAE has become a key decision point for anyone planning to buy property in 2026, especially in a market where financing options are more competitive, flexible, and digitally advanced than ever before. A right mortgage choice can significantly impact your long-term financial comfort, monthly repayment structure, and overall property investment success in the UAE.

Mortgage solutions across UAE banks now offer tailored packages for residents, expats, and investors with varying income levels and property goals. Understanding how interest rates, eligibility criteria, repayment flexibility, and bank reputation work together helps you make a more informed and financially secure decision before committing to any home loan agreement.

What Makes a Bank the Best for Mortgage Loans in UAE?

Choosing the right mortgage lender isn’t just about the lowest interest rate. The best banks in the UAE offer a combination of competitive pricing, flexible repayment terms, transparent fees, and strong customer support. Factors like fixed vs variable rates, loan tenure (up to 25 years), early settlement charges, and approval speed all play a critical role in your decision.

Additionally, top-performing banks align their offerings with UAE Central Bank regulations, ensuring safe lending practices. They also provide value-added services such as pre-approval, online mortgage calculators, and dedicated relationship managers, making the home financing process smoother for buyers.

Top Banks for Mortgage Loans in UAE (2026)

Emirates NBD

Emirates NBD is one of the most popular choices for mortgage loans in the UAE, known for its competitive interest rates and flexible loan structures. It offers both fixed and variable rate options, making it suitable for first-time buyers and seasoned investors alike.

The bank also provides quick pre-approval processes and strong digital support, which simplifies the application journey. With high loan-to-value (LTV) ratios and tailored solutions for expats, Emirates NBD remains a leading option in 2026.

ADCB (Abu Dhabi Commercial Bank)

ADCB stands out for its attractive fixed-rate mortgage plans and low processing fees. It is particularly appealing for buyers who want predictable monthly payments over the initial years of their loan.

In addition, ADCB offers excellent customer service and flexible repayment options. Their mortgage solutions cater to both salaried and self-employed individuals, making them a reliable choice for diverse financial profiles.

Dubai Islamic Bank

Dubai Islamic Bank is ideal for buyers seeking Sharia-compliant home financing. Instead of traditional interest-based loans, it offers Islamic mortgage solutions like Ijara and Murabaha.

These options provide ethical and transparent financing structures, which are increasingly popular in the UAE market. The bank also offers competitive profit rates and flexible tenures, making it a strong contender in the mortgage sector.

Mashreq Bank

Mashreq Bank is known for its fast approval process and digital-first approach. It offers competitive mortgage rates and personalized loan packages based on the applicant’s income and property type.

With innovative features such as online application tracking and flexible repayment terms, Mashreq appeals to tech-savvy buyers who want convenience without compromising on value.

Mortgage Loan Requirements in UAE

To qualify for a mortgage loan in the UAE, applicants must meet certain eligibility criteria set by banks and the UAE Central Bank. Typically, you need a stable income, a minimum salary (usually AED 10,000+), and a good credit score. Expats and UAE nationals may have slightly different requirements, especially in terms of down payment.

Banks also evaluate your debt-to-income ratio, employment stability, and property valuation before approving the loan. Preparing documents such as salary certificates, bank statements, and identification in advance can significantly speed up the approval process.

Interest Rates and Loan Types Explained

Mortgage loans in the UAE generally come with two main types of interest rates: fixed and variable. Fixed rates offer stability for a set period (usually 1–5 years), while variable rates fluctuate based on market conditions and the EIBOR rate.

Choosing between these options depends on your financial strategy. Fixed rates are ideal for predictable budgeting, while variable rates may offer savings if market rates decrease. Understanding these options helps you align your mortgage with your long-term financial plans.

Key Tips to Choose the Right Mortgage Bank

When selecting the best bank for your mortgage loan, consider more than just the headline interest rate. Look at the total cost of borrowing, including processing fees, insurance, and early settlement penalties.

Also, evaluate the bank’s reputation, customer service, and flexibility in repayment. A slightly higher rate from a reliable bank with better service can often be more beneficial in the long run than a cheaper but rigid option.

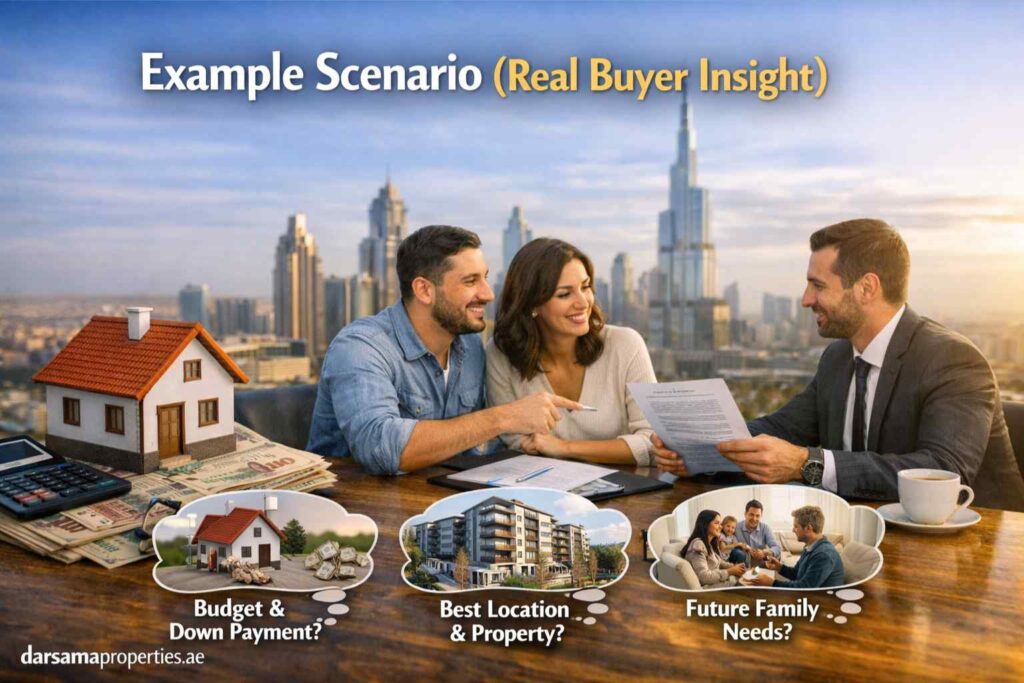

Example Scenario (Real Buyer Insight)

Imagine a buyer earning AED 20,000 per month looking to purchase a property worth AED 1 million. With a 20% down payment, they would need a mortgage of AED 800,000. Choosing a bank with a 4% fixed rate vs 5% can save thousands over the loan tenure.

This example highlights how small differences in mortgage terms can significantly impact your financial outcome. That’s why comparing multiple banks and understanding the fine print is crucial before making a decision.

Also Read: Mortgage Companies in Dubai for Expats & Investors

Conclusion

Best bank for mortgage loan in UAE depends on how well a bank aligns with your income stability, repayment capacity, property goals, and long-term financial planning, as every lender offers different advantages in terms of interest rates, flexibility, and approval conditions across the UAE mortgage market in 2026.

Right mortgage decision can create long-term financial ease and stronger property investment outcomes when all factors such as loan tenure, hidden charges, and rate structure are properly evaluated before final commitment.

Start your property journey with expert guidance from darsamaproperties.ae today and get the right mortgage support for smarter real estate investment in UAE.

FAQ About Best Bank For Mortgage Loan

Q1: What is the best bank for mortgage loan?

Ans: The best bank for mortgage loan depends on interest rates, approval speed, repayment flexibility, and customer support offered by the lender.

Q2: How to choose the best bank for mortgage loan?

Ans: Choose the best bank for mortgage loan by comparing interest rates, loan terms, processing fees, and eligibility requirements carefully.

Q3: Which bank gives the lowest mortgage loan interest rate?

Ans: The bank offering the lowest mortgage loan interest rate varies by country, credit score, and loan type, so comparison is essential.

Q4: Is it better to get a mortgage loan from a bank or lender?

Ans: A bank is often safer for mortgage loan due to regulated terms, lower interest rates, and long-term repayment stability.

Q5: What documents are needed for a mortgage loan?

Ans: For a mortgage loan, banks typically require ID, income proof, property documents, credit history, and employment verification.

Q6: How can I get approved for a mortgage loan easily?

Ans: You can improve mortgage loan approval chances by maintaining a good credit score, stable income, and low debt-to-income ratio.